Bucharest Real Estate: The Market Nobody Is Talking About Honestly

21 May 2026 • Imobiliare

This article is for informational purposes only and does not constitute legal, tax, or financial advice. For specific situations, consult a qualified professional.

A recent conference on Romanian real estate delivered competent analysis. Familiar names, familiar arguments, familiar conclusions. Supply is tight. Prices are high. Political instability is to blame.

All true. All incomplete. The real estate market in Bucharest and Ilfov is more complex — and more fragile — than the industry narrative currently acknowledges. This is our reading of it.

The Scarcity Argument Has a Shelf Life

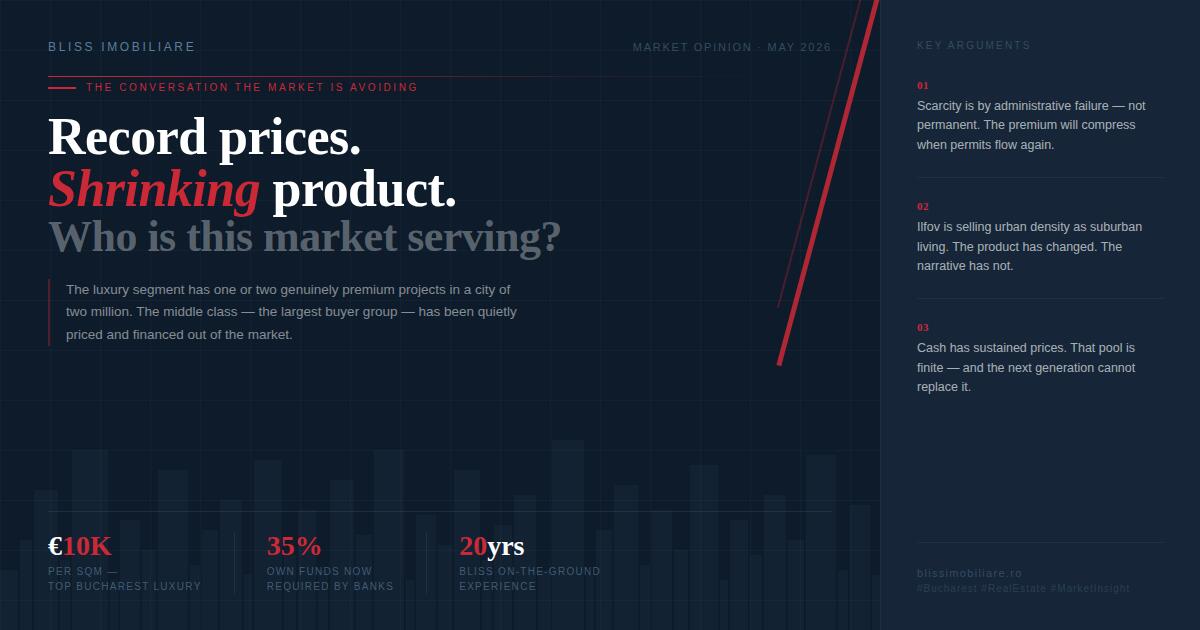

Luxury prices in Bucharest have reached €10,000 per square metre in the best locations. One or two projects in a city of two million people can genuinely claim premium positioning. That is a real anomaly — and yes, prices reflect it.

But the comparison made at the conference — that a scarce Bucharest apartment resembles a Brâncuși sculpture in its uniqueness — confuses two very different things. A sculpture is rare by creation. A premium apartment is scarce by administrative failure. One holds its premium permanently. The other holds it until the political blockage clears, permits flow again, and supply returns.

Buyers paying top-of-market today are paying for a regulatory window. They should know that.

Ilfov: The Same Story, A Different Product

The early 2000s Ilfov boom was real. Families left Bucharest for houses in Voluntari, Pipera, Tunari, and Otopeni. They bought space, privacy, gardens, a different pace of life. Plots of 500 to 800 square metres. Homes of 180 to 250 square metres built area. The product delivered what it promised.

What is being built in the same corridor today is sold under the same narrative — and delivers something fundamentally different. Plots of 150 to 250 square metres. Homes of 100 to 130 square metres. Neighbours three metres away on either side. That is not suburban living. That is urban density with a symbolic garden.

The economics are straightforward. Land that cost €5 to €15 per square metre in 2003 now costs €80 to €200 depending on location. Developers compressed the product to protect margin. Permissive local planning enabled it. And buyers accepted it — because the reference point was always the Bucharest apartment they were leaving, not the genuine house they believed they were buying.

These developments will age. In ten to fifteen years, when the original buyer wants to move on, resale differentiation will be difficult. The product will not clearly separate itself from the apartment market it was meant to replace. Infrastructure — roads, schools, utilities — is already visibly strained. That deficit compounds quietly, and eventually shows up in valuations.

The Largest Segment Is Being Ignored

Every conference panel discussed investors, yields, capital appreciation, and high-net-worth mobility. Not one focused seriously on the segment that actually drives residential market volume: the middle-income family looking for a home.

Not a portfolio asset. Not a yield play. A home.

This segment is being squeezed from both sides simultaneously. Prices have risen sharply across all categories. At the same time, access to financing has tightened structurally — banks requiring 25% to 35% own funds contributions, stricter debt-to-income ratios, and higher mortgage rates. A household that qualified for a property loan five years ago may no longer qualify for the same property today. That is not a cycle. That is a structural exclusion of the market's largest natural buyer group.

The investor mentality has colonised what is, for most families, the most important financial decision of their lives. Developers build for investors. They price for investors. They communicate for investors. The result is a market that serves a minority efficiently while the majority is priced out or underserved.

Investor-driven markets are also fragile markets. They move on sentiment and liquidity. A market anchored by owner-occupiers — people who bought homes to live in, not to exit — is fundamentally more resilient. Romania's residential sector has been moving in the opposite direction for years.

Cash Has Been King. The Question Is What Comes Next.

Romanian real estate has sustained elevated prices partly because of an unusually high proportion of cash transactions. Accumulated savings, inheritance, capital from business activity — this domestic liquidity pool has kept demand active even as mortgage accessibility declined.

But cash pools are finite. The next generation of buyers has genuine housing needs and limited inherited liquidity. They cannot participate in a market priced for cash buyers and calibrated to investor returns. As the current generation deploys its capital, the structural question becomes unavoidable: what sustains demand at current price levels when that pool is exhausted?

The early signals are already there — in longer time-on-market for mid-range properties, and in the growing gap between asking price and transaction price in the €100,000 to €200,000 segment.

A market that excludes its largest natural buyer group cannot maintain its current trajectory indefinitely. That is not a forecast. It is arithmetic.

The Signal Worth Taking Seriously

The one genuinely important observation from the conference — that Romania's wealthiest individuals are increasingly directing capital abroad in search of predictability — was raised and then moved past. It deserves more than a footnote.

When the high-net-worth segment systematically exits, you are not looking at a real estate problem. You are looking at a country confidence problem. That requires a harder conversation than the industry is currently willing to have.

Where This Leaves the Market

Premium Bucharest supply constraints are real and will sustain current price levels — until they do not. The political blockage will eventually resolve. Supply will return. The uniqueness premium will compress.

Ilfov is delivering volume on a value proposition it can no longer fully support. The product has changed. The narrative has not.

The middle-income segment — the foundation of any healthy residential market — is structurally underserved, underfinanced, and absent from the conversations that shape policy and development strategy.

And the cash-driven demand that has kept the market moving is a finite resource with no clear successor in sight.

This is not a market in crisis. But it is a market building on foundations that deserve more scrutiny than they are currently receiving.

BLISS Imobiliare has been active in the Bucharest and greater Ilfov residential and premium property market since 2006. Our perspectives are based on direct transaction experience, client advisory, and two decades of on-the-ground observation.

For enquiries: [email protected] | blissimobiliare.ro